Revenue, expense, and capital withdrawal (dividend) accounts are temporary accounts that are reset at the end of the accounting period so that they will have zero balances at the start of the next period. Closing entries are the journal entries used to transfer the balances of these temporary accounts to permanent accounts.

Revenue, expense, and capital withdrawal (dividend) accounts are temporary accounts that are reset at the end of the accounting period so that they will have zero balances at the start of the next period. Closing entries are the journal entries used to transfer the balances of these temporary accounts to permanent accounts. After the closing entries have been made, the temporary account balances will be reflected in the Retained Earnings (a capital account). However, an intermediate account called Income Summary usually is created. Revenues and expenses are transferred to the Income Summary account, the balance of which clearly shows the firm's income for the period. Then, Income Summary is closed to Retained Earnings.

The sequence of the closing process is as follows:

Close the revenue accounts to Income Summary.

Close the expense accounts to Income Summary.

Close Income Summary to Retained Earnings.

Close Dividends to Retained Earnings.

The closing journal entries associated with these steps are demonstrated below. The closing entries may be in the form of a compound journal entry if there are several accounts to close. For example, there may be dozens or more of expense accounts to close to Income Summary.

1. Close Revenue to Income Summary

The balance of the revenue account is the total revenue for the accounting period. Since revenue is one of the components of the income calculation (the other component being expenses), in the last day of the accounting period it is closed to the Income Summary account as follows:

Closing Entry : Revenue to Income Summary

| Date | Accounts | Debit | Credit |

| mm/dd | Revenue | xxxx.xx | |

| Income Summary | xxxx.xx |

Once this closing entry is made, the revenue account balance will be zero and the account will be ready to accumulate revenue at the beginning of the next accounting period.

2. Close Expenses to Income Summary

Expenses are the other component of the income calculation and like revenue, are closed to the Income Summary account:

Closing Entry : Expenses to Income Summary

| Date | Accounts | Debit | Credit |

| mm/dd | Income Summary | xxxx.xx | |

| Expenses | xxxx.xx |

After closing, the balance of Expenses will be zero and the account will be ready for the expenses of the next accounting period. At this point, the credit column of the Income Summary represents the firm's revenue, the debit column represents the expenses, and balance represents the firm's income for the period.

3. Close Income Summary to Retained Earnings

The income or loss for the period ultimately adds to or subtracts from the firm's capital. The Retained Earnings account is a capital account that accumulates the income from each accounting period. The Income Summary account is closed to Retained Earnings as follows:

Closing Entry : Income Summary to Retained Earnings

| Date | Accounts | Debit | Credit |

| mm/dd | Income Summary | xxxx.xx | |

| Retained Earnings | xxxx.xx |

4. Close Dividends to Retained Earnings

Any capital withdrawals (e.g. dividends paid) during the period will reduce the capital account balance, so the withdrawal is closed to Retained Earnings:

Closing Entry : Dividends to Retained Earnings

| Date | Accounts | Debit | Credit |

| mm/dd | Retained Earnings | xxxx.xx | |

| Dividends | xxxx.xx |

After closing, the dividend account will have a zero balance and be ready for the next period's dividend payments.

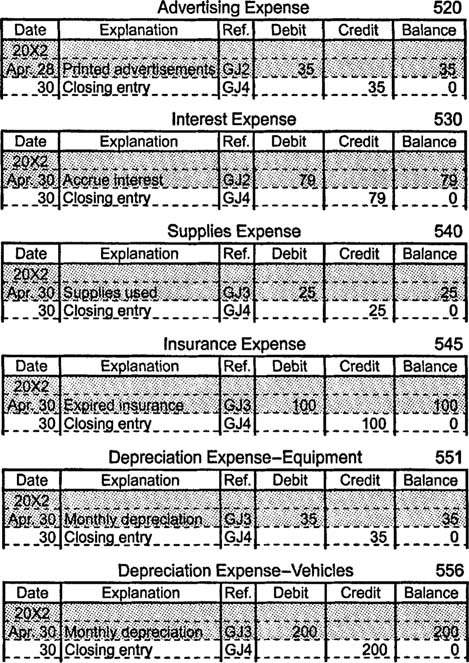

Posting of the Closing Entries

As with other journal entries, the closing entries are posted to the appropriate general ledger accounts. After the closing entries have been posted, only the permanent accounts in the ledger will have non-zero balances.

Post-Closing Trial Balance

Once the closing entries have been posted, the trial balance calculation is performed to help detect any errors that may have occurred in the closing process.

No comments:

Post a Comment